Key Characteristics

Non-traded debt issued by specialized funds

Direct lending to middle-market companies ($25-75M EBITDA)

Customized terms and flexible documentation

Higher yields to compensate for illiquidity

Private credit refers to debt securities that are not publicly issued or traded, where specialized investment funds lend directly to businesses outside the traditional banking system¹. Non-bank lenders provide customized financing solutions primarily to small and middle-market companies that lack access to public bond and loan markets². This direct relationship allows for faster execution, flexible terms, and stronger borrower control compared to traditional bank lending.

Sources:

1. National Association of Insurance Commissioners, Capital Markets Bureau, Private Credit Primer. NAIC, 2024, Analysts, Jennifer Johnson and Michele Wong

2. Global Private Markets Report 2024: Private markets: A slower era [Report],”McKinsey & Company, March, 2024

Non-traded debt issued by specialized funds

Direct lending to middle-market companies ($25-75M EBITDA)

Customized terms and flexible documentation

Higher yields to compensate for illiquidity

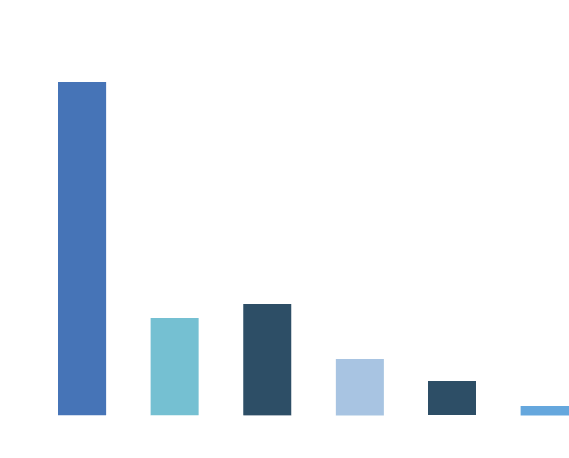

Six Core Strategies Driving Market Diversification

Private credit has evolved beyond traditional corporate lending into diverse strategies serving different market needs. Corporate lending dominates at 54%³, but the market is rapidly diversifying. According to NAIC and Preqin analysis, six key strategies define the modern private credit landscape¹, each targeting specific borrower types and risk-return profiles.

Sources:

1. National Association of Insurance Commissioners, Capital Markets Bureau, Private Credit Primer. NAIC, 2024, Analysts, Jennifer Johnson and Michele Wong

3. Financing the Economy 2024, ACC

The Players: Who Makes Private Credit Happen

This interconnected ecosystem has created a ~$3 trillion⁴ alternative asset class that delivers faster execution, customized solutions, and higher yields than traditional banking. The specialized division of roles attracts pension funds, insurance companies, and sovereign wealth funds seeking returns unavailable in public markets.

Sources:

4. Financing the Economy 2024, ACC.

Asset managers, institutional investors, family offices. provide capital and seek strong risk-adjusted returns. They face challenges with opaque markets, manual processes, and illiquid holdings that limit portfolio flexibility.

Loan originators, direct lenders, banks, and specialty finance firms create and issue private credit assets outside traditional banking. They struggle with inefficient capital raising, complex compliance requirements, and limited investor transparency.

Custodians, administrators, and technology providers handle compliance, settlements, and reporting. Current systems are manual and fragmented, creating inefficiencies and higher costs that slow transactions.

Private credit has exploded from $200 billion in 2009 to $3 trillion today⁴—driven by bank regulatory retreat, private equity demand, and institutional investor appetite. Apollo forecasts the market could reach $40 trillion by 2030⁵, while the current market represents only 4.5% of the overall US credit market¹, indicating massive expansion potential across infrastructure, real estate, and asset-based financing.

Sources:

1. National Association of Insurance Commissioners, Capital Markets Bureau, Private Credit Primer. NAIC, 2024, Analysts, Jennifer Johnson and Michele Wong

5. Bloomberg, Apollo Says Private Credit May Reach $40Trillion by 2030, Dec 19, 2024

Current Market Size

Market Potential

AI, Blockchain & Retail Access Transforming the Market

Technology is democratizing private credit for individual investors. 63% of firms now use AI⁶ for smarter underwriting, while blockchain enables fractional ownership of institutional assets. Private wealth vehicles hold $400B+ AUM⁴, with Blackstone's BCRED ($66.6B) leading retail access.

Sources:

4. Financing the Economy 2024, ACC.

6. Broadridge "Transforming Private Credit with AI" 2024

AI, Blockchain & Retail Access Transforming the Market

Private credit operates under lighter oversight than banks, but regulatory pressure is building⁽¹²⁾.

Fifth Circuit ruling limits regulatory reach (June 2024)

FSOC monitoring opacity and interconnectedness

Bank capital requirements accelerating private credit growth (July 2025)

European regulators developing parallel frameworks

Sources: 12. SEC Investment Advisers Act Rules; FSOC 2024 Annual Report; Basel Committee Publications

This podcast aims to share discussions and insider takes into the private credit asset class. Delivered by industry experts.

Watch Now

A collection of podcasts on various private credit topics. Features interviews with industry leaders and covers various topics.

Watch Now

Explore the shift in the private credit environment with alternative asset managers are moving quickly to unlock capital.

Watch Now

Build a 360° view of the private markets with new and insightful perspectives from industry thought leaders.

Watch Now

An accessible primer on private credit vehicles, structure, return-risk profile and key risks.

Learn More

A BIS Quarterly Review article analyzing cross-border growth patterns, financial-stability implications, and the evolving role of private credit funds.

Learn More

A selection of industry reports on private credit including a survey on LPs perspective on private markets including private credit.

Learn More

GPCA is the authoritative, non-commercial provider of research on private capital activity and trends in global markets.

Learn More

Research paper discussing the potential risk to the financial system that the growth of private credit may bring.

Learn More

A proposal by the FSB on policy recommendations to enhance monitoring and contain leverage risk in private credit and other Non Bank Financial Institution (NBFI) activities

Learn More